A trust is a fiduciary arrangement that allows a third party, or trustee, to hold and manage assets on behalf of one or more beneficiaries.

Trusts are attractive estate planning tools because they usually avoid probate and enable efficient and cost-effective transfers of assets. Certain irrevocable trusts may also avoid estate and gift taxes.

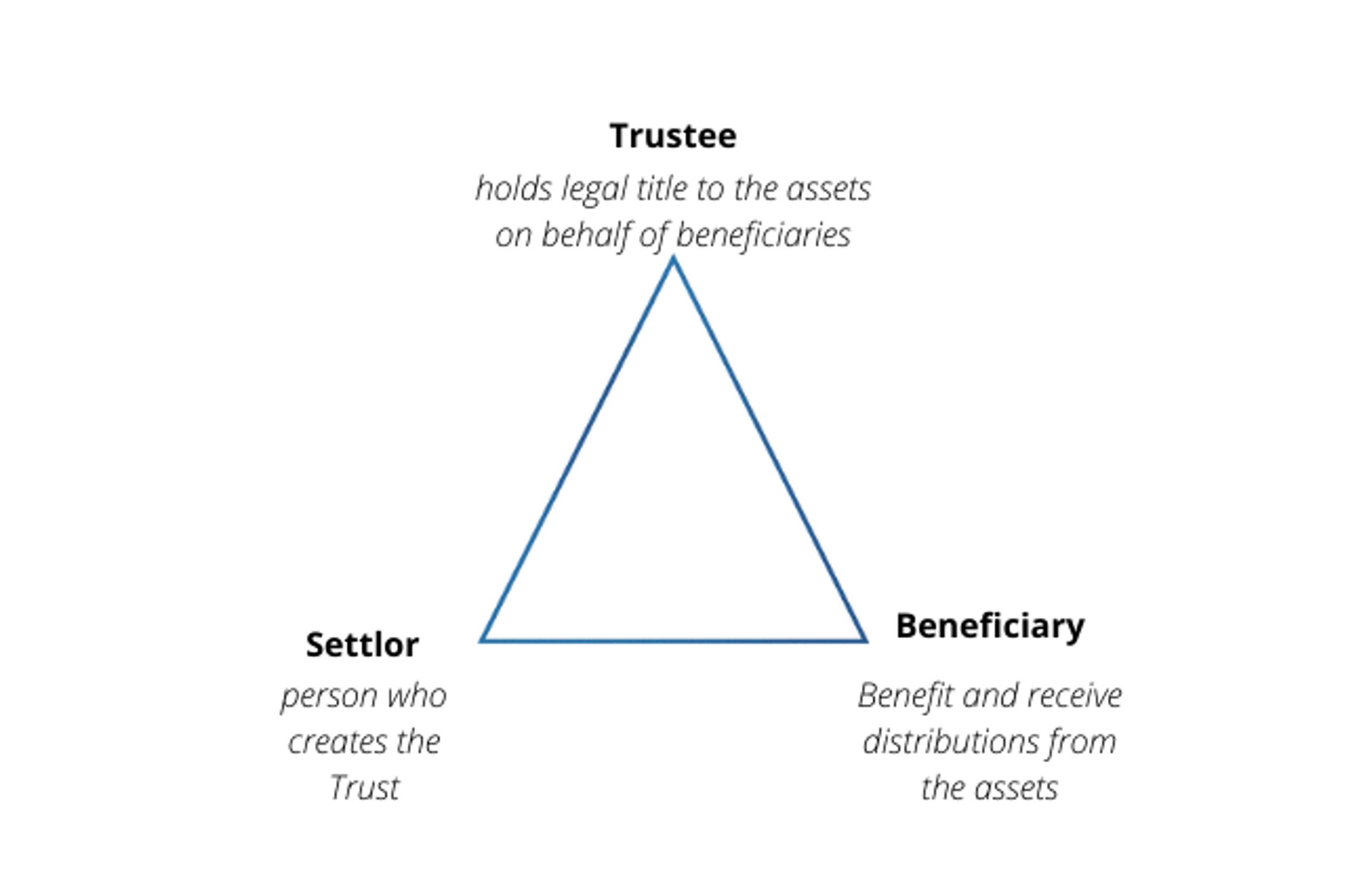

Key Players in a Trust

There are three main players in a trust: the person who creates the trust, the trustee, and the beneficiaries.

The person who creates a trust is called the “Settlor.” The terms “Creator”, “Grantor,” “Donor,” and “Trustor” are also sometimes used and accepted without any different legal significance.

The “Trustee” of a trust is the person who holds legal title to the trust property on behalf of the trust beneficiaries. A Trustee is somewhat analogous to the Executor or Personal Representative of a last will, except that the Trustee holds legal title to the trust property and serves during the lifetime of the Settlor.

The Beneficiaries of a trust are the ones who stand to benefit from or inherit the trust’s assets.

Revocable vs. Irrevocable Trusts

There are many different kinds of trusts tailored for various purposes, but they all fall into one of two major categories:

- Revocable Living Trusts

- Irrevocable Trusts

Revocable living trusts are trusts in which the person creating the trust (the Settlor) retains the ability to modify or cancel the trust. As a result of this trait, the IRS considers property held by the revocable living trust to continue to be owned by the Settlor. This means that you’ll report any income or capital gains on revocable living trust assets directly on your individual or joint tax return in the same manner that you do today.

Unlike revocable living trusts, irrevocable trusts cannot be altered or cancelled after they are created. Therefore, when a Settlor creates an irrevocable trust and transfers assets out of the estate and into the trust, the trust assets are typically no longer considered property of the Settlor. This may put the assets outside the reach of creditors and estate taxes.

When should you use a revocable living trust or an irrevocable living trust?

For most people who simply want to avoid probate or benefit from any of the other non-tax advantages of trusts, revocable living trusts are a better fit than irrevocable living trusts. The flexibility to modify or cancel a revocable living trust makes them better adapted to possible changes in your life or desires.

There are only three motivations for which you should consider creating and funding an irrevocable living trust:

- To minimize estate taxes

- To become eligible for need-based government programs and assistance

- To protect your assets from creditors

You can learn more here how an irrevocable trust can fulfill these three motivations. It’s worth noting, however, that creating and funding an irrevocable trust is not the exclusive means of achieving these outcomes.

For example, if you are concerned about paying estate taxes, you can implement a wide variety of advanced tax strategies to reduce or eliminate your estate tax liability without necessarily needing to create an irrevocable trust.

If you work in a profession that frequently faces lawsuits like surgeons or real estate developers, you might consider purchasing liability insurance in addition to or in lieu of transferring your assets to an irrevocable asset protection trust.

What’s the best way to create a trust?

You can create a revocable living trust by yourself, with the help of an estate planning attorney, or through a digital service like Just In Case Estates. Most people do not need an attorney to create a revocable living trust, and therefore online trustmakers like Just In Case Estates provide the best value.

If you fall into one of the three exceptions for which an irrevocable trust may make sense, you should engage an estate planning attorney specialist for 1:1 legal advice. Your estate planning attorney can help make sure that you fully understand your irrevocable trust and how to properly fund and maintain it. Irrevocable trusts are permanent – there’s no way to change one once it’s executed and funded. Additionally, transfers to irrevocable trusts are usually subject to gift tax, and while there are ways around paying the gift tax, you should work with your attorney to set up a plan that’s right for you.