Irrevocable trusts are trusts that cannot be altered or cancelled after they are created. In an irrevocable trust created and funded during the creator’s lifetime, funding the trust transfers assets out of the estate and potentially outside the reach of creditors and estate taxes.

Do I need an irrevocable trust?

For most people who simply want to avoid probate or benefit from any of the other non-tax advantages of trusts, revocable living trusts are a better fit than irrevocable living trusts. The flexibility to modify or cancel a revocable living trust makes them better adapted to possible changes in your life or desires.

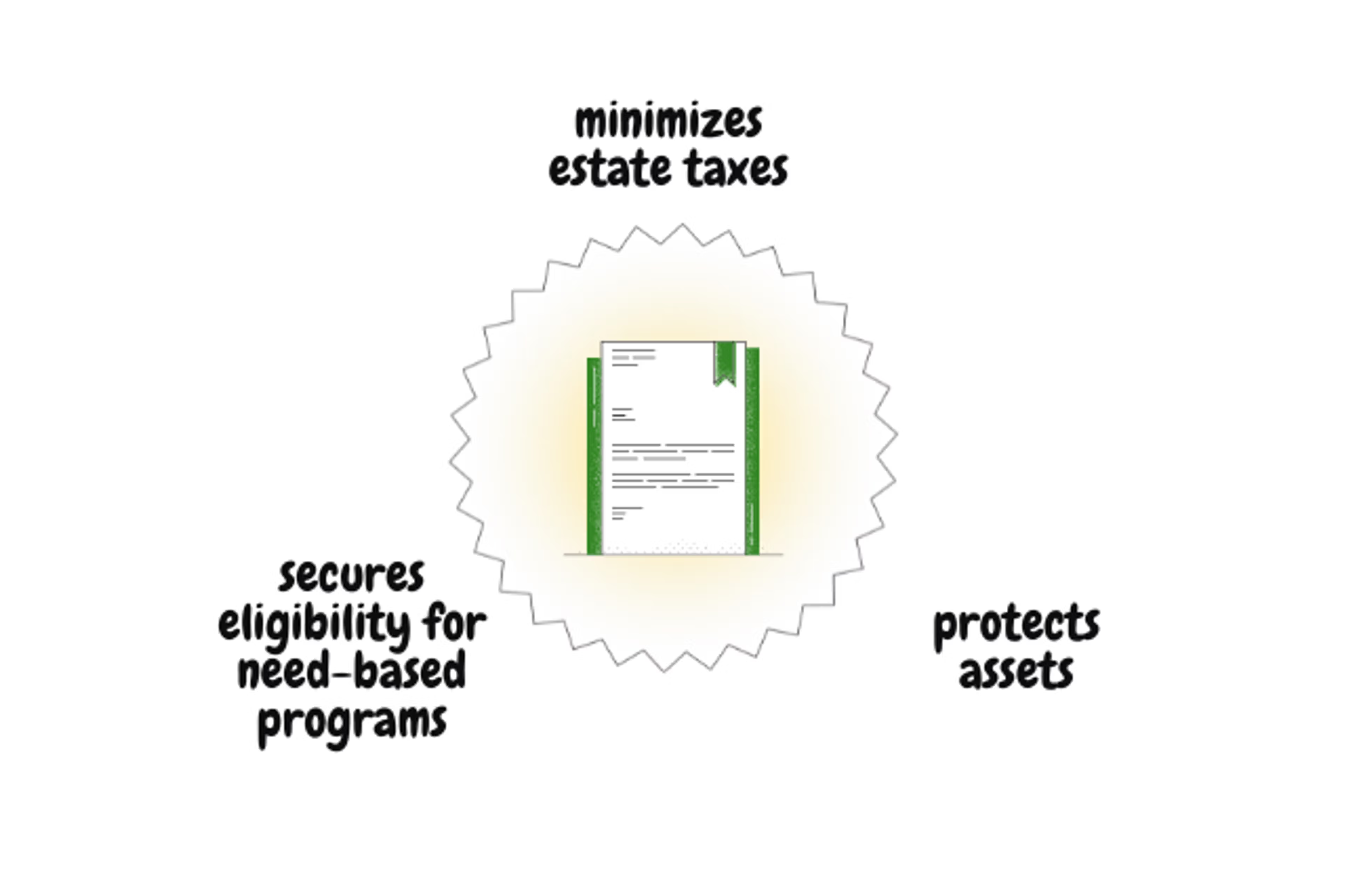

There are only three instances in which you should consider creating and funding an irrevocable living trust:

- Minimizing estate taxes

- Becoming eligible for need-based government programs and assistance

- Protecting your assets from creditors

Let’s take a close look at how an irrevocable trust accommodates each of these three needs.

| Revocable Living Trust | Irrevocable Living Trust | |

|---|---|---|

| Ability to make changes to or revoke the trust | ✔ | |

| Avoids estate taxes | ✔ | |

| May gain eligibility for need-based programs | ✔ | |

| Protects assets from creditors | ✔ |

#1 Minimizing Estate Taxes

Irrevocable living trusts transfer assets out of the ownership and control of the person creating the trust, and therefore property held in irrevocable trusts is usually not included in calculation of the creator’s gross estate for estate tax purposes.

The ‘catch’ is that if your irrevocable living trust’s beneficiaries are individuals, the amount funded to the irrevocable trust is normally considered a “gift” to the beneficiaries and therefore triggers the gift tax.

One creative way that estate planning attorneys and accountants have gotten around this gift tax trigger is by including a provision in the irrevocable trust document that allows beneficiaries to withdraw the contributions made to the trust for a limited amount of time (i.e., 30 days after funding). This potential to withdraw funds, known as a “Crummey Power”, creates a “present interest” of the beneficiary in the trust funds, which allows the contributions to qualify for the gift tax exemption. So long as the contributions per beneficiary are less than the gift tax threshold in a given year ($16,000 in 2022), the contributions to the irrevocable living trust are both estate and gift-tax free.

A second workaround to the gift tax trigger is to utilize the lifetime gift exemption. Instead of paying gift tax in the year that the Settlor makes the contribution to the irrevocable trust, the Settlor files a gift tax (Form 709) electing to have the gift value deducted from the Settlor’s lifetime gift threshold. As long as the Settlor doesn’t use up all of his or her exemption amount, the estate won’t have to pay federal gift tax on the gift now or in the future. This strategy works well with assets that are anticipated to quickly increase in value, because the value of the gift and reduction in the lifetime gift threshold is the asset’s current, lower value at the time of funding as opposed to its presumably much higher value upon subsequent distribution.

#2 Becoming Eligible for Need-Based Government Programs and Assistance

Medicaid and Supplemental Security Income provide benefits to disabled or special needs individuals, but in order to qualify for these programs, those individuals have to meet strict income and asset limitations. If such an individual makes or owns too much money, that individual may fail to qualify for the programs and lose the benefits.

By transferring assets or income of the disabled or special needs individual into an irrevocable trust, those funds are no longer considered property of the individual. This setup allows the individual to receive the ‘core’ benefits of the government-funded program for free, with the trust picking up the bill for any benefits or needs that are not funded by the program.

#3 Protecting Your Assets from Creditors

Individuals who have a lifestyle or career that makes them high targets for lawsuits may turn to a special type of irrevocable trust, called an asset protection trust, to move assets out of reach of potential creditors, lawsuits, and judgments.

In this irrevocable trust model, the person who creates the trust is the beneficiary. The trust dictates that if the creator becomes subject to a lawsuit or likely to lose a creditor judgment, the trustee is prevented from distributing any of the assets or income of the trust to the creator. This “spendthrift” provision makes the trust assets and income inaccessible to the other party.

Not all states allow the creation of Domestic Asset Protection Trusts. For this reason, these types of trusts are often created in states that have trust-friendly laws like Delaware, Nevada, South Dakota, and Tennessee.

Alternatives to Irrevocable Trusts

Due to the permanent nature of irrevocable living trusts and the potentially complex setup required, you should engage an estate planning attorney if you are considering creating an irrevocable living trust.

Your estate planning attorney can also speak with you about potential alternatives to irrevocable trusts that are more flexible and may still meet your needs. For example, if you are concerned about paying estate taxes, you can implement a wide variety of advanced tax strategies to reduce or eliminate your estate tax liability without necessarily needing to create an irrevocable trust. If you work in a profession that frequently faces lawsuits like surgeons or real estate developers, you might consider purchasing liability insurance in addition to or in lieu of transferring your assets to an irrevocable asset protection trust.