A revocable living trust is a legal instrument that acts as a will substitute to efficiently transfer assets at death.

Although a revocable living trust requires more upfront and regular maintenance compared with a last will, many individuals prefer using a revocable living trust as the core of their estate plan because it allows you to avoid probate and its associated cost.

Read on to learn everything that you need to know about revocable living trusts, or take our estate plan matching quiz to determine whether a revocable living trust is right for you.

Key Players in a Revocable Living Trust

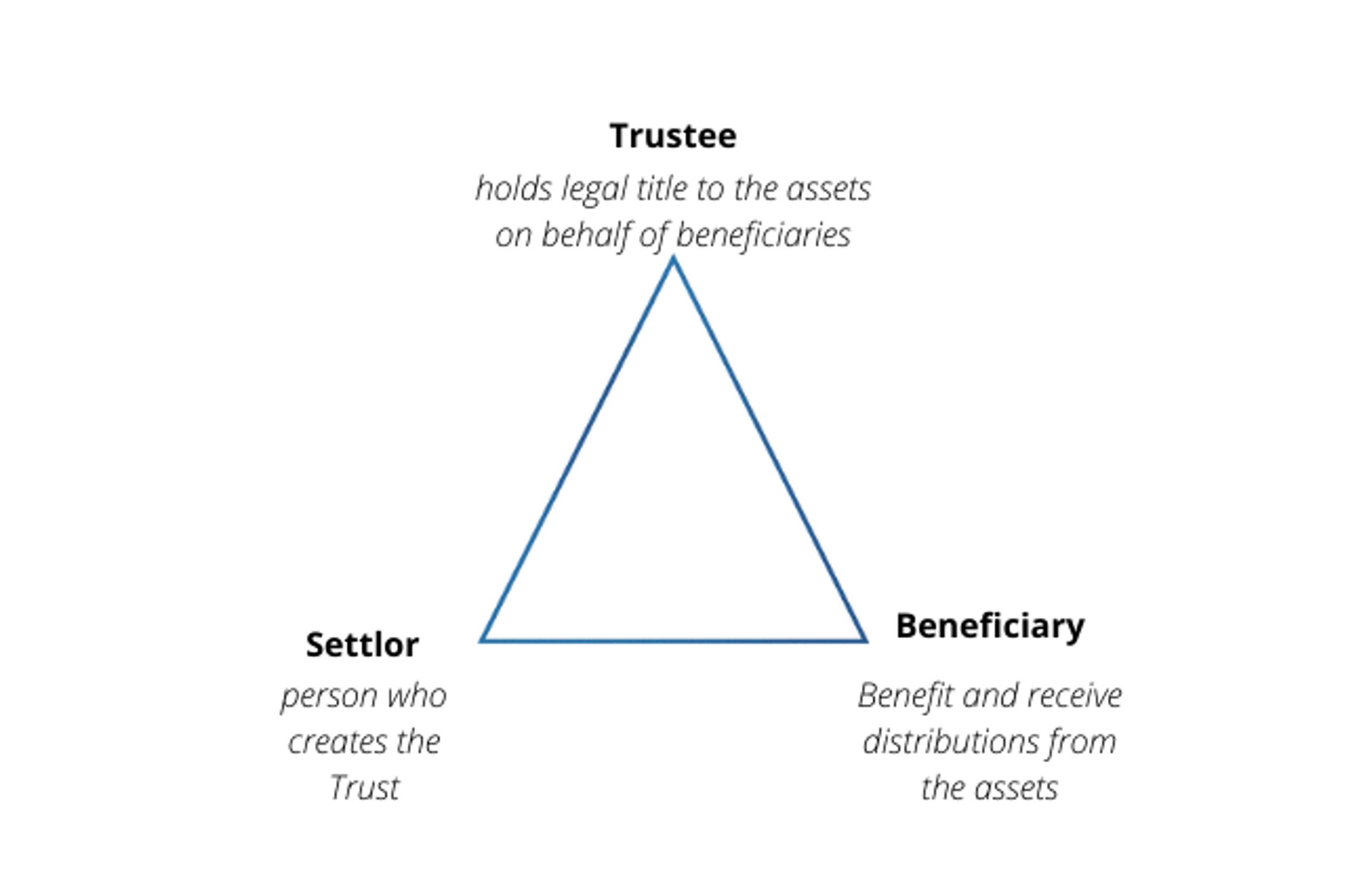

There are three main players in a revocable living trust: the person who creates the trust, the trustee, and the beneficiaries.

The person who creates a revocable living trust is called the “Settlor.” The terms “Grantor,” “Donor,” and “Trustor” are also sometimes used and accepted without any different legal significance.

The “Trustee” of a trust is the person who holds legal title to the trust property on behalf of the trust beneficiaries. A Trustee is somewhat analogous to the Executor or Personal Representative of a last will, except that the Trustee holds legal title to the trust property and serves during the lifetime of the Settlor. The Settlor is often the initial Trustee or Co-trustee of the revocable living trust during the Settlor’s lifetime.

The beneficiaries of a trust are the ones who stand to benefit from or inherit the trust’s assets.

How Does a Revocable Living Trust Work?

After drafting and executing a revocable living trust agreement, the next step is to fund the trust by transferring the Settlor’s assets into the trust. During the Settlor’s lifetime, the Settlor retains complete control over the trust property and can change any of the terms of the trust or revoke it in its entirety.

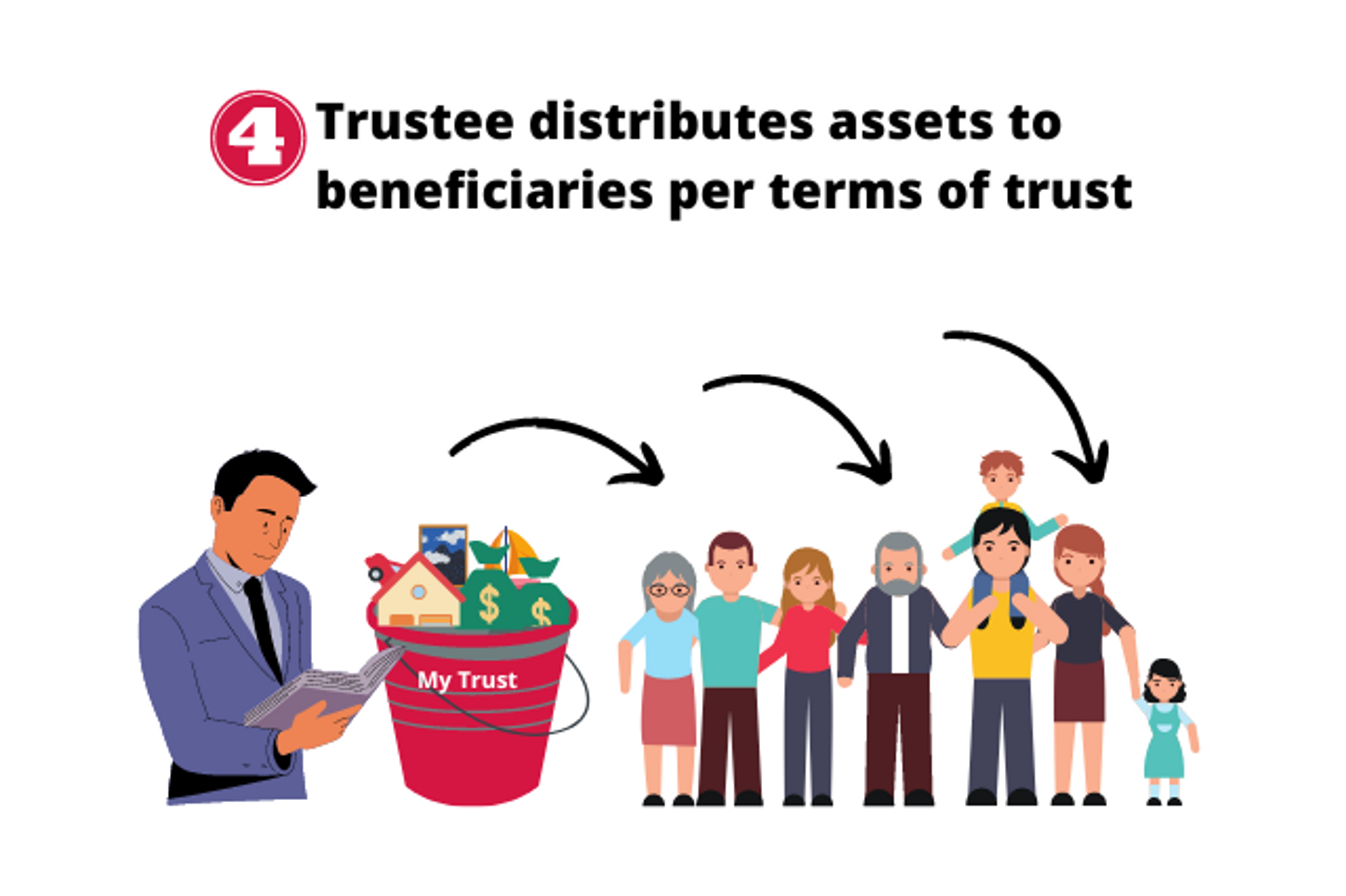

Upon the death of the Settlor, the trust becomes irrevocable, and the successor Trustee named in the trust takes over management of the trust. A pour over will, often created in tandem with a revocable living trust, helps transfer any leftover assets into the trust that for whatever reason weren’t funded into the trust during the settlor’s lifetime. With all the assets now held by the trust, the successor trustee distributes the trust assets to the trust beneficiaries according to the terms of the trust.

After creating the trust document, you fund the trust by re-titling assets in the name of the trust.

During your lifetime, you can continue to buy, sell, receive income from, and use the assets just as you did before.

Upon your death, a Pour Over Will "pours over" or funds any leftover assets that weren't yet titled in the name of the trust into the trust.

Your trustee follows the instructions in your revocable living trust to make distributions to your beneficiaries.

What are the advantages of using a revocable living trust?

A revocable living trust plan enables you to do everything that you can do in a will, and then some. There are four primary advantages of using a revocable living trust as the core of your estate plan:

- Avoids probate. Unlike last wills, trusts do not need to go through the probate process. This helps make asset transfers upon death more efficient and estate administration less costly compared to administration with a last will.

- Maintains privacy of the estate plan. Since trusts don’t go through probate, estate administration with a trust does not create a public record in the same way that estate administration with a last will does. This helps keep the nature of the gift and other provisions in your trust private.

- Offers greater control over timing and conditions for gift distributions. With a revocable living trust, you can keep your assets “in trust” to distribute on an as-needed basis or on the completion of various milestones. For example, you could specify that a person should receive a gift after reaching a certain age or that a beneficiary can only use funds for a limited set of purposes like higher education, medical expenses, or maintaining a certain standard of living.

- Avoids guardianship during the settlor’s lifetime. Holding your assets in a revocable living trust can avoid guardianship proceedings, the process by which the court determines who should manage your personal property, if you become incapacitated or otherwise unable to manage your own affairs.

What are the disadvantages of using a revocable living trust?

The primary disadvantage of using a revocable living trust is that it requires more upfront setup and ongoing maintenance compared to a last will.

Upfront Setup

After you complete and properly execute your trust, you need to fund the trust by transferring your assets into the trust. The process to fund a trust is not particularly difficult, but it does take time and coordination with multiple third parties.

You don't have to fund all of your assets into the trust on day one. A good strategy is to make a list of the assets that you want to transfer into the trust, and start with the highest value assets and work your way down.

Ongoing Maintenance

Tax treatment for property held in a revocable living trust is the same as if you held it directly, because the IRS considers the power to revoke a revocable living trust as grounds that it continues to be owned by the Settlor (you) (I.R.C. § 676(a)). This means that you’ll report any income or capital gains on trust assets directly on your individual or joint tax return in the same manner that you do today.

Although tax treatment of property held in a revocable living trust is the same, you’ll nonetheless need to create a listing of the trust assets and keep trust property separate from other property that you own. As you acquire or sell property, you’ll need to make changes to the list and remember to title newly acquired property in the name of the trustee. Similar to the initial funding of a revocable living trust, none of this ongoing maintenance is particularly difficult, but it does require attention and care.

How much does a revocable living trust cost?

The cost of creating a revocable living trust varies depending on a number of different factors.

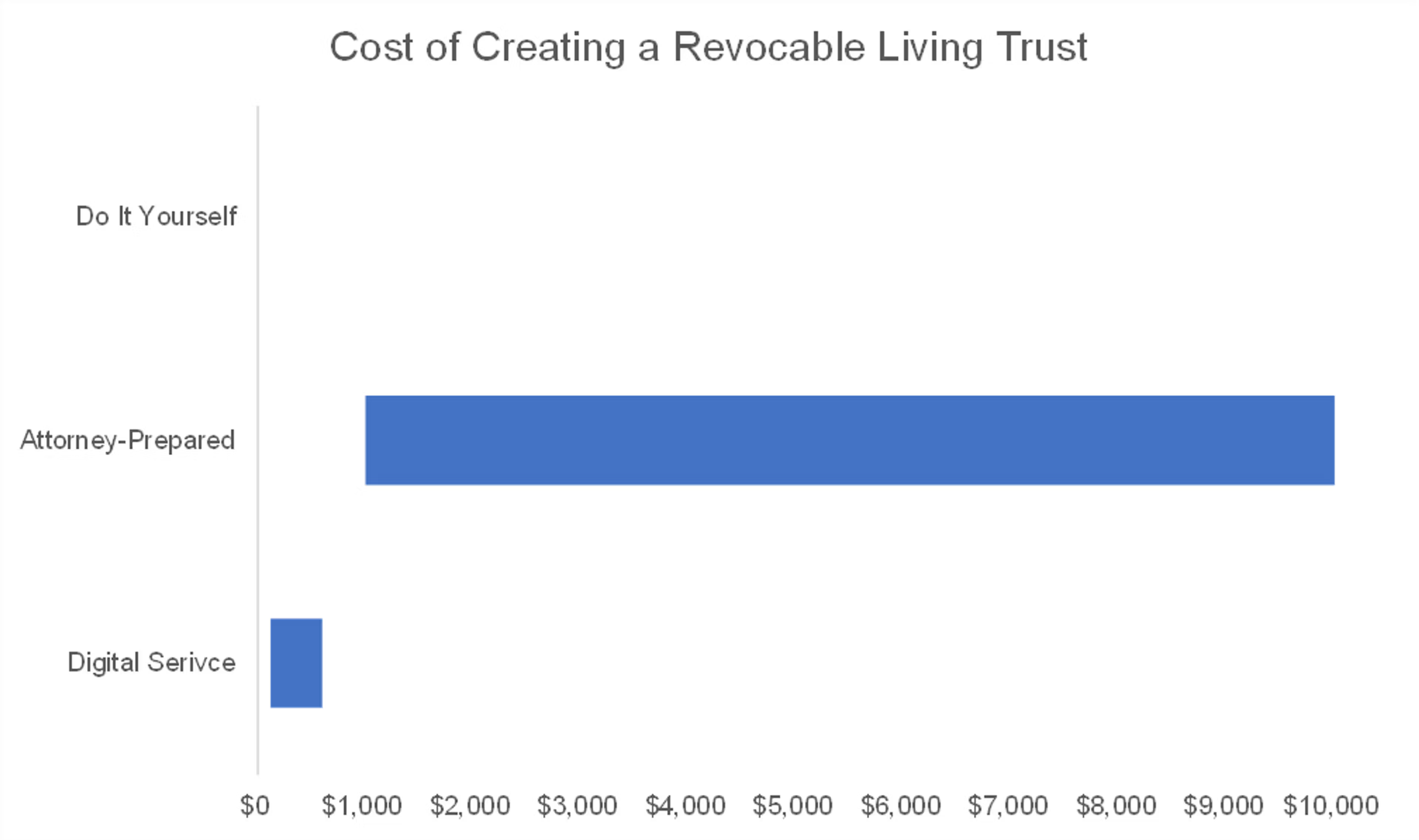

There is no legal requirement that you create a revocable living trust with an attorney. Unless you are already familiar with your state’s trust laws or plan to do independent research, however, the time and energy exhausted by creating your trust independently are unlikely to be worth the savings.

The cost of attorney-prepared revocable living trusts ranges from $1,000 to $10,000. Expect to pay on the higher end of this range if any of the following apply to your situation:

- You are making a revocable living trust for a couple (vs creating only one individual trust)

- You opt to create your trust with a more experienced estate planning attorney

- You live in a large metropolitan area

- You have a lot of beneficiaries, or you want to establish complex conditions regarding gift distributions

- You want your attorney to help fund your trust for you

The cost of preparing a revocable living trust through an online trustmaker is much more straightforward and typically a flat fee ranging from $120 to $600. Service providers on the lower end of this price range typically offer only the revocable living trust form with little to no additional support. On the upper end, you may be able to meet virtually with an attorney to ask questions about your situation and plan.

Just In Case Estates is priced in the middle with revocable living trusts starting at $348 for individuals and $448 for couples. When you choose Just In Case Estates for your revocable living trust, you’ll get premium live support from our customer success team to help guide you through the process of creating and funding your revocable living trust. You’ll also receive access to our member portal, where you can easily make updates to your plan and collaborate with your trustees, financial and other advisors, and even a third-party estate planning attorney if you have one now or in the future. When it comes time to administer your estate, your trustee has everything that the trustee needs to fulfill his or her duties at the fingertips.

Do I need a revocable living trust?

Choosing to create a revocable living trust or a last will is a personal decision driven by how you much value the advantages of a revocable living trust versus the higher setup and ongoing maintenance requirements.

As a general rule of thumb, if your total assets are less than $100k in value with a relatively simple asset structure, you probably don’t need a revocable living trust and may even qualify for an expedited small estate probate proceeding in your state. As your assets increase in value, the complexity of your assets increases, or you want greater control and privacy, a revocable living trust makes more sense.

If you need help deciding whether a revocable living trust or a last will is right for you, you can chat with our customer success team or see our recommendation by taking our estate plan quiz.